Technology is rapidly transforming the insurance industry, but there’s one technology that is proving more crucial than any other.

The number of blockchain applications in insurance grows every day, and it’s clear that within the next few years, every major player in the space will be using them in some way.

This creates massive opportunities for fintechs, as well as for smaller insurance companies willing to embrace the change.

In this extensive guide, we’ll look at some of the most popular and most innovative blockchain insurance applications, and how you can benefit.

Keep reading, and you’ll find out:

- What is blockchain, exactly?

- The incredible security implications of DLT.

- How blockchain will benefit every sector of the industry, from life, to health, to title, and automotive.

- Real-life blockchain insurance use cases that are generating massive buzz.

- How you can join them.

- And how Ignite can help.

What Is Blockchain

Although blockchain has been all over the news in recent months, the mainstream conversation has largely been about Bitcoin and other cryptocurrencies.

The truth is, blockchain has applications that go far beyond financial instruments, and could be transformative to industries ranging from law enforcement, to manufacturing, and even insurance.

Although there are plenty of guides available for those new to the idea, a quick primer is in order before discussing how blockchain will affect the insurance industry in particular.

At its core, blockchain is a way to safely store data. Another name for blockchain is distributed ledger technology, or DLT, and this is a better descriptor of how the tech works.

The Chain Analogy

The easiest way to think about blockchain is right in the name. The technology works much like a physical chain, albeit one made of data.

Each link in the chain is called a block, and is owned by a specific user.

If a user is authorized, then they can add a link to the chain, meaning they add data in the form of a block.

Once that block is added, then it’s just like adding a link to a physical chain. It’s irrevocably attached to the blocks before and after it.

In digital terms, this means that every block is hashed to the blocks that precede it.

To put it in very simple terms, the blocks are encrypted with a security key that is based on the blocks before it.

What this means is that it’s nearly impossible to hack a blockchain. Just as in removing a link from a physical chain would be instantly obvious to anyone looking, so too does altering data in a blockchain.

This is extremely important, and there’s another analogy that can help us understand how.

The Dollar Bill Analogy

Let’s think about it in terms of cryptocurrency, like bitcoins. That was the original application of blockchain, and it’s a useful launchpad before talking about other applications.

Each individual bitcoin is secured by hashing it to the blocks preceding it in the chain. This makes them extremely difficult to crack, but the real magic happens when combined with the transparency of the chain.

Anyone can look at a coin and see who owns it (though generally in the form of an anonymizing wallet address).

When a bitcoin changes owner, such as during a financial transaction, then the new wallet address is public information.

The net effect of all this is to make bitcoins function very much like physical currency. If you hold a dollar bill in your hands, anyone can look and see that you own that dollar.

If dollars were traditional data, then they could snap their fingers and copy that dollar.

On blockchain, that’s impossible. And if someone were to reach out and take that dollar, you would instantly know, and so would anyone else who was watching.

It creates a level of inherent trust.

Perfect Security for Data Management

Currency isn’t the reason blockchain is such a buzzword this year, though. The entire tech industry, from startups to massive institutions, are throwing themselves at new DLT applications.

IBM alone has opened a new 1,000-employee office in Munich dedicated to blockchain, funding it with $200mm.

The market for blockchain technologies is predicted to exceed $7.5 billion by 2024.

The reason for this is that innovators have already seen the massive possibilities of blockchain.

By taking the concepts of the distributed ledger and applying them to information other than financial instruments, DLT can be used to power applications in literally any industry.

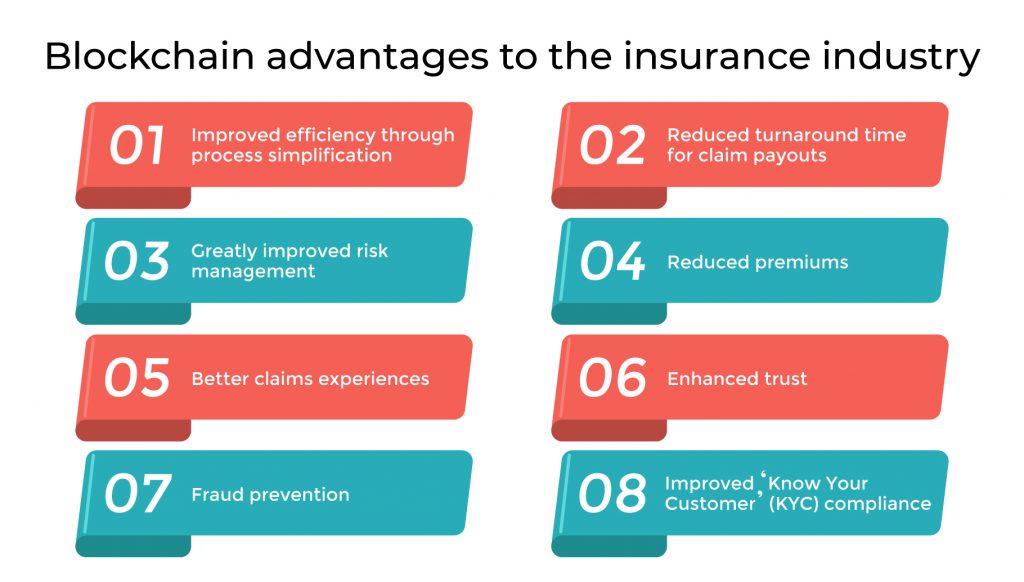

Blockchain Insurance Applications

For insurance, as with most industries, the power of blockchain lies in cutting out the middleman.

With so much personal data at stake, the insurance industry is currently bogged down by countless checks and rechecks.

When all that information is on a blockchain, virtually all those checks can be dispensed with. Information is trusted and can flow directly from one party to the other.

The savings in both time and money are astronomical, and that is what’s transforming the industry.

Let’s look at how blockchain will touch some of the largest sectors in insurance.

Blockchain in the Life Insurance Industry

For life insurance, blockchain has implications at every step of the process.

Rates

Due to the inherent security of the distributed ledger, new clients can be quoted and onboarded faster than ever before.

When blockchain is fully integrated into the industry, prospective clients will be able to unlock access to their own medical histories so that a carrier can generate a quote automatically.

The lengthy process of gathering documents from various doctors and medical professionals will be no more. Everything will be in the cloud, trusted and secure.

Claims

In the United States alone, there are estimated to be $7.4 billion in unclaimed life insurance money.

People spread apart, papers are lost, and in the hustle and bustle of life, sometimes it’s not possible to find the proper beneficiary for a claim.

With blockchain-based smart contracts, this problem can finally be addressed.

Funds could automatically and proactively be paid out based on news of a death, without waiting for the beneficiary to come forward with a claim.

Trades

It’s something of an open secret that life insurance policies can be traded and sold like many other financial instruments. If an insured no longer requires the insurance, but has paid the premium, they may sell the policy and benefits for immediate cash, to whomever they like.

Selling a policy is a complicated process that goes through several intermediaries. Luckily, eliminating intermediaries is where blockchain shines.

In future, insured people will be able to sell their policies at will, quickly and easily.

Blockchain in the Health Insurance Industry

Many of the same aspects of blockchain also apply to health insurance, plus a few that are unique to this sector of the industry.

Medical Records

DLT will be a boon to medical professionals everywhere. By making a patient’s medical records immutable, digitally accessible, and transparent, medical error will practically be a thing of the past.

Because blockchain is also incredibly secure, medical fraud and privacy violations should also decrease dramatically.

For insurance agents and carriers, generating quotes will be an easy, automatable process, with instantaneous access to all the necessary records to provide accurate rates.

Claims

As with life insurance, smart contracts will enable claims to paid out quickly and automatically.

When a patient checks into a hospital, treatment records will automatically be added to the blockchain, and the insurance company will pay out.

The need for complicated forms and back-and-forth communication will be drastically reduced.

Reduced Costs

Doctors, administration, and insurers alike will all see a massive efficiency boost from blockchain.

With complete and trusted access to a patient’s complete medical history across all providers, doctors will be able to see and utilize the results of tests made at other facilities, without complicated requests for information.

They will be able to consider the results of past procedures, eliminating the duplication of work that is so common today. Treatments will take less time and involve less trial-and-error. All of this means that medical costs will go down, and that’s to the benefit of everyone.

Blockchain in the Title Insurance Industry

Perhaps more than any other sector, blockchain has the power to completely disrupt title insurance.

If you’re not familiar, title companies are a critical piece of any real estate transaction. They verify that deeds and other documents are transferred properly, that mortgages are processed, and that records are kept.

In other words, they make sure everyone dots the I’s and crosses the T’s, every step of the way.

Title insurance is a protection against an error anywhere in that process.

If a person buys a house, or a company buys a property, it’s not unheard of for a dispute to come up from someone who claims they have an interest in the real estate, and that it’s not a legal sale until they get paid.

Other common disputes include such matters as property lines, public easements, or inheritances. These are known as title defects, and they can crop up even years after the sale.

The effects of blockchain on this problem are obvious. Most, if not all, title defects stem from some failure in documentation or record-keeping.

Real estate transactions are incredibly complicated, and a missing link anywhere along the paper trail can spell disaster.

With blockchain, there are no more missing links. If property records are moved to distributed ledger, then fraud and tampering become a thing of the past, as does missing information.

What’s more, smart contracts are cutting out the middleman in businesses all over the world. If titling becomes a quick and easy affair, without the possibility of error, then there is no more need for traditional title insurance at all.

So, what will happen to the title insurance providers? They’ll need to adapt. Here are two roles that they might fill in the coming blockchain insurtech ecosystem.

Edge Cases

A blockchain of property deeds will account for most potential threats to a transaction, but it can’t account for everything. Bankruptcy, divorces, court cases, and financial debts can all affect a sale, and they won’t all go on a blockchain reserved for real estate matters.

For these, human oversight will still be required.

Legacy Systems

Digital records are catching on fast in the United States, with several states even offering electronic notarization of documents. However, there are still many places worldwide that are still working with paper documents, or non-connected computer systems.

Until every county and municipality has moved to the cloud, there will still be a place for title companies.

Blockchain in the Auto Insurance Industry

Automotive insurance is one area where blockchain is already taking a firm hold. There are startups already leveraging it to great success, as you’ll see below.

This is one of the largest sectors in insurance, with more people carrying auto policies than life or health. The companies are motivated to find new ways to both lower premiums and increase profits, and blockchain is one of the keys.

Here’s how.

Fraud Prevention

Insurance fraud is an ever-present issue in the auto industry, costing as much as $80 billion per year in the US alone. It’s common for bad actors to try to claim for the same damage twice, or for vendors to overbill for simple repairs.

With blockchain, this becomes much more difficult. If a vehicle’s repair record is linked to the chain, then it is sacrosanct. Claims are cross-referenced to previous claims, repairs, and even accident photos, making verification automatic and near-instantaneous.

Traffic Data

With blockchain, AI, and big data analytics, premiums can be calculated more accurately than ever before. Traffic conditions, accident frequency, current events, and even an insured’s own driving habits can all contribute to an incredibly precise risk assessment.

Good drivers being penalized for their demographic will become a thing of the past.

Speed

With the possible exception of health insurance, auto insurance currently requires more middlemen than any other sector. When a claim is filed, it must be verified by the police, the motor vehicle administration, repair shops, the other driver, their insurance, and more.

With blockchain, all the necessary information can be distributed instantly and simultaneously. The lengthy back-and-forth between all interested parties can end, and that will save everyone money.

A claim will be as simple as checking the blockchain for the accident’s effects, and then making the payout.

Insurance Companies Using Blockchain Today

None of this is theoretical. Blockchain isn’t a trend to watch, to see if it will catch on.

It’s something that’s really happening, right now.

Let’s look at four companies that are already disrupting the industry through the use of distributed ledger technology.

Kasko2Go

Sector: Automotive

Insurance tech startup Kasko2Go is making waves in the insurtech space for being the first to market with a fully blockchain-based automotive insurance solution.

Using DLT, AI, and other cutting-edge techniques, Kasko2Go is able to eliminate most of the red tape that surrounds traditional auto insurance. Every insured vehicle is assigned a unique ID, essentially making it a link in the blockchain.

The claims process is as simple as sending a photo of the accident. Kasko2Go uses public data sources to verify the incident immediately and automatically, sending a payment on the claim in about 30 minutes.

The best part? All of those savings allow Kasko2Go to run on a comparatively tiny budget and pass those savings on to the insured. Their premiums run up to 50% less than the industry average.

The company has even dipped into the cryptocurrency space. Their crypto token, the K2G, is available now. It’s based on the Ethereum blockchain and will help fund the company as it grows.

fidentiaX

Sector: Life

Web: https://www.fidentiax.com/

As mentioned, it’s a little-known fact that life insurance policies can be sold by their owners, typically the insured.

It’s common for a policy to be “paid-up”, meaning the insured has paid enough premiums into it that no more are due for some time, even years.

This is convenient, but it can lead to some awkward situations. If someone’s life circumstances change through divorce or a death in the family, then they may have a policy but no beneficiary.

In these cases, there used to be no feasible recourse. Policies are non-refundable. They can be sold, but the process is time-consuming, complicated, and error-prone.

An insurance startup called fidentiaX plans to change that, using blockchain to streamline the procedure.

Policies will be tokenized and placed on a distributed ledger, allowing for fast and easy transactions. By eliminating the slew of intermediaries needed in a traditional policy sale, they allow policyholders to trade and sell almost as easily as putting up an item on eBay.

In fact, fidentiaX structures their site very much like the auction giant, with a simple online marketplace. It’s a little morbid, but undeniably effective.

Everledger

Sector: Personal Property

Web: https://www.everledger.io/

Everledger has cornered a small but valuable niche in the insurance sector: diamonds.

More and more, the value of a diamond is tied to its provenance and grading.

A handful of institutions, primarily the Gemological Institute of America, grades stones as they enter the marketplace.

Flaws, clarity, and several other factors are scrutinized by experts. Many of those factors are difficult to detect by the layman.

At the same time, an increasing sense of social responsibility means that “blood diamonds”, referring to diamonds mined through slave labor or in untenable work conditions, are dropping in value.

Unfortunately, there’s no way to tell a blood diamond simply by looking at it. Buyers must simply take the supplier at their word and hope that the merchant shares their principles.

Until now.

Using blockchain, Everledger today delivers secure and trusted reports for stones directly to consumers. Graders upload their reports onto the ledger, where they are tied to individual stones, making the physical objects part of the chain.

It’s the first time that consumers can look up for themselves whether a diamond meets their quality and moral standards, and it’s already proving to be a gamechanger.

Everledger completed a $10.8mm funding round in 2018.

They plan to use the money to expand their operations by diversifying into other gemstones, and into certification of fine wines.

Etherisc

Sector: Trip

Combining blockchain with big data analytics, Etherisc is helping protect one of the most common investments in the world: plane tickets.

Their signature product, Flight Delay, allows consumers to insure that their finances aren’t disrupted even if their travel plans are. A policy covers a single flight. If the flight is delayed by 45 minutes or more, then it immediately pays out.

For the consumer, it couldn’t be simpler. On the back end, it’s revolutionary.

This type of insurance has been available in the past through traditional insurance, but it’s been bogged down with endless fees, paperwork, and delays.

By tokenizing policies and proactively checking flight data, Etherisc takes control of the process.

Policyholders don’t need to file claims to collect on a delayed flight. Etherisc emails them first, letting them confirm the delay and receive their payout within minutes. Everything is automatic, saving time and money over manually processed claims.

Flight Delay is fully licensed and available today.

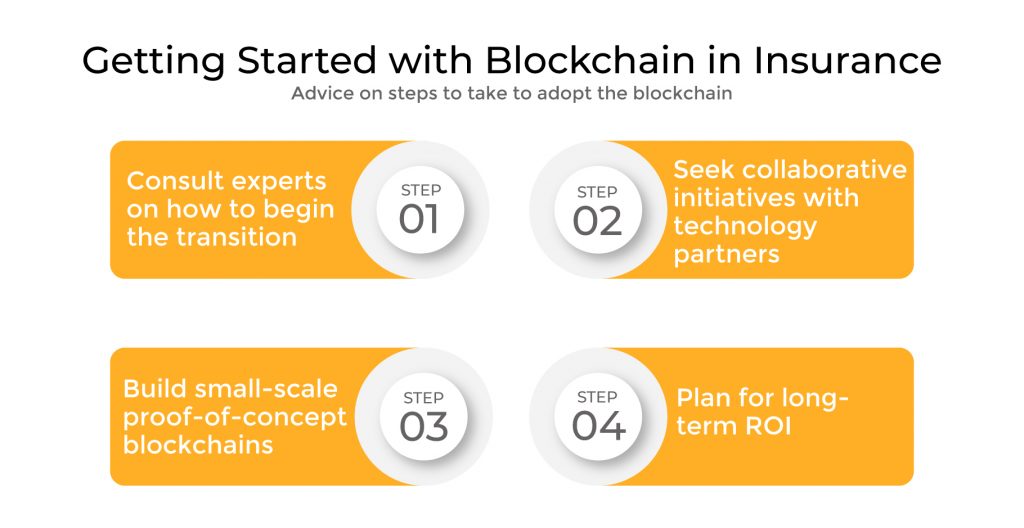

How to Leverage Blockchain Today

For insurance professionals and tech entrepreneurs alike, there are many opportunities surrounding blockchain insurance applications. Here are a few roles that will need to be filled in days to come.

Consultancy

Blockchain as a technology is still in its infancy, having only been first described in 2008. Today, many people are familiar with cryptocurrency thanks to the bitcoin boom, but the other applications of DLT are still relatively unknown.

Insurance agencies and carriers are starting to wake up to the fact that they just don’t know what’s possible. The potential benefits of blockchain, as well as the potential threats to their traditional business models, are still largely mysterious to them.

They will need people to educate them on the new blockchain reality, and they’ll be willing to pay.

Technology Partners

As with any technological revolution, there’s a great market for talented software development. However blockchain’s disruption of insurance shakes out, the one sure thing is that it will require a great deal of new software.

Customer-facing websites, mobile apps, back-end quoting systems, vendor management, and of course the blockchains themselves. All of this will need tech professionals familiar with DLT, and used to working with cutting edge, still-developing mechanisms.

The most successful innovators will find themselves inundated with work, as their reputation spreads. Once the largest players in the insurance space catch on, and they will, then enormous contracts or even acquisitions will be on the table.

Blockchain-Based Insurance Companies

There’s a widening niche for insurance companies to base their entire business around distributed ledgers.

Blockchain makes possible entirely new ways of thinking about insurance. It allows for entirely customer-driven quoting, as clients can customize their policies to a degree heretofore unheard of.

It even allows for the worldwide spread of microinsurance, the concept of very small insurance policies that is already a way of life in India.

In the developed world, such policies would cost more in terms of labor than they are worth.

With blockchain, that’s no longer the case. There’s plenty of room for startups to bring creative new forms of insurance to the industry, experiencing explosive growth and profitability before the established giants catch up.

How Ignite Can Help

When it comes to cutting-edge technology, Ignite is one of the best software development houses in the world.

Founded in Ukraine and today operating in Israel, Ukraine, and across Europe, the company has over 150 successful projects to its name.

Ignite is more than comfortable working with new tech, having made its name in virtual reality, augmented reality, IoT, and more.

Now, the firm has staffed up with some of the best blockchain talent in the world and stands ready to take your ideas from inception to market.

Whether your business is an insurance agency hoping to modernize your approach in a rapidly-changing market, or a fintech looking for support in bringing your latest idea to life, Ignite can help.

By leveraging the power of outsourcing and Agile development, you can work within a razor-thin budget without sacrificing quality of work. At every step of the way, your Ignite team will be in close contact with you, ensuring that your vision is maintained.

If you’d like a free consultation to find out what Ignite can do for you, fill out the form below. A project manager will be in touch with you shortly to discuss next steps.